The Tomb We Built

There are two kinds of pain.

There is acute pain, the kind you feel all at once. It is loud, it is obvious, and it forces you to deal with reality immediately. It is a burn from a hot stove.

Then there is chronic pain, the kind you feel every day. It is quieter, it is persistent, and it slowly changes the way you move through the world. You stop taking risks. You stop running. You stop believing the pain will ever go away. You become a shell of your former self. You lose your ambition, your appetite.

Crypto has normalized chronic token unlocks, yet we act surprised when the market starts walking with a limp.

Crypto is supposed to be an infinite game. New players can join at any time. New narratives can emerge overnight. I wrote about this last year, and I still believe it, but there is a design choice we keep making that quietly turns the infinite game into something finite, predictable, and miserable for anyone who is not already in.

We build tombs. We build them with token unlock schedules, and then we move into them.

Specifically, the four year monthly unlock. A gentle, responsible, professional-looking drip that is supposed to feel fair and stabilizing, but in practice becomes a permanent headwind that restricts new buyers, suffocates marginal demand, and anchors price lower for longer than almost anyone expects.

Most people talk about token unlocks like they are the weather. They’re something that just happens, or a future problem on the calendar.

In reality, unlocks are closer to a recurring capital raise. Every unlock is a moment where the market has to re-underwrite the project, again, and again, and again, even if nothing about the product has changed. New supply always shifts market structure. Tokens then have to compete on the least annoying dilution, as opposed to the best product or metrics.

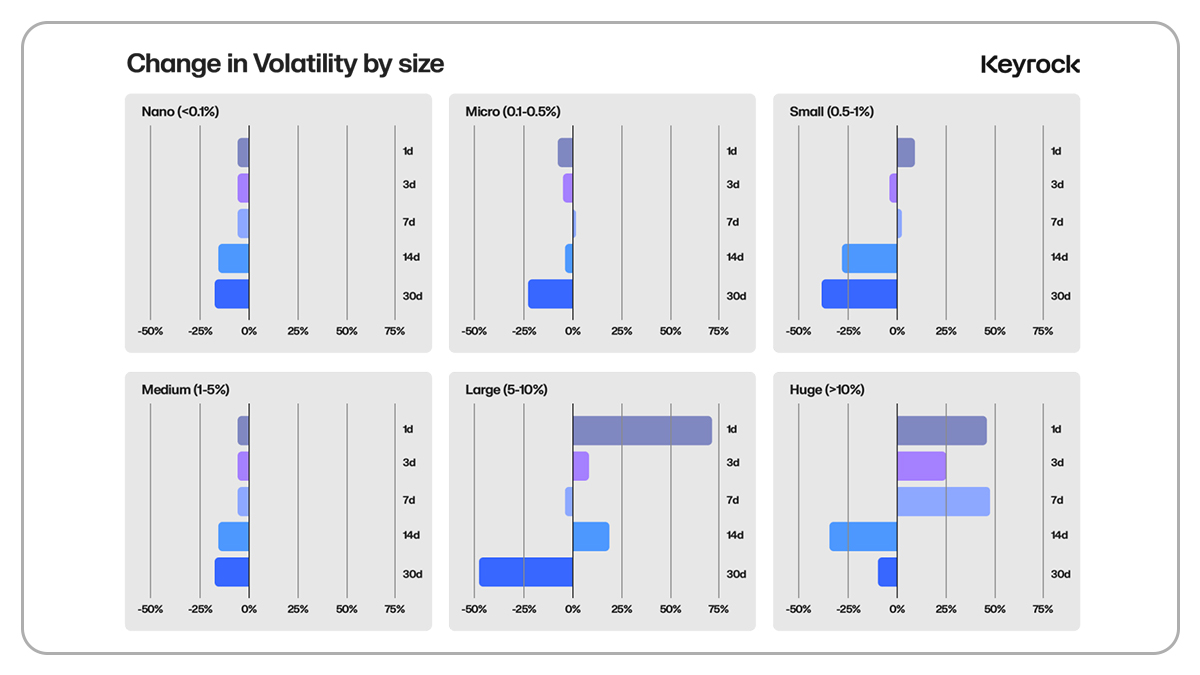

Keyrock analyzed more than 16,000 token unlock events and the conclusion is not subtle: unlocks are usually negative for price. They report that 90% of unlocks create negative price pressure, and that price impacts often start 30 days before the unlock event.

This behavior is not restricted to tokens; IPOs also see a similar increase in trading volume and negative returns around their initial unlocks (which typically last around 180 days). In The Expiration of IPO Share Lockups by Field & Hanka, they studied 1,948 IPOs and found a permanent ~40% increase in trading volume, and a statistically significant 3-day abnormal return of around 1.5%. More recent analysis suggests that unlock returns are closer to -9%.

In crypto, we take this phenomenon and replay it 36 times. Frequency matters.

When you scale for relative size, unlocks can look similar in terms of suppression. Frequency becomes the more telling factor, and Keyrock observes consistent downward pressure from smaller, steady unlocks. “Massive unlocks cannot be entirely hedged due to their size and cannot be dumped or unwound within 30 days. As a result, their market effects tend to be more gradual and drawn out.”

The art of the slow bleed

Token price is set at the margin. The marginal buyer is the new buyer, the person who does not already have a position and is deciding whether to start one.

Now imagine you are that person. You like the product, the team, and even the valuation.

You then learn that for the next 36 to 48 months, a predictable chunk of new supply is coming every single month. The market has to absorb it. Someone has to buy it, and you have no guarantee that the project will create new demand at the same rate supply increases.

What do you do?

You wait.

Or you trade it tactically and refuse to marry it (most people are here).

Or you buy something else where the supply schedule is not an ever-present tax on holding (the rest of the world is here).

This is why long linear unlocks restrict new buyers. They turn the act of buying into a commitment to be that month’s exit liquidity, unless demand grows fast enough to offset the constant issuance. This is also why you often see liquid funds playing within the wake of initial unlocks for 12 months before moving onto the next token. It’s an easier game to play when you avoid misaligned timelines and incentives.

Buyers are not irrational, they are simply responding to market structure. The drip teaches people to fade rallies, and once a market learns that behavior, it is very hard to unlearn. It doesn’t help that all of the charts look the same.

Let’s check the math

Time for a thought experiment.

Assume a token has a $1B market cap. Assume it has a monthly unlock equal to 1% of total supply. Imagine price is flat.

That means the market needs to absorb roughly $10M of incremental supply value every single month just to keep the price where it’s at. Not to go up, just to not go down. If you don’t believe me, here are some more examples.

Arbitrum: a multi year monthly overhang

Arbitrum is one of the clearest examples of how a long monthly schedule can become the dominant narrative.

ARB is vesting at a monthly rate of 108.6 million ARB, about 1.1% of total token supply, with allocations fully vesting by March 2027.

Regardless of what you think about Arbitrum as a network, you can see the structural problem for price formation.

A buyer is not underwriting Arbitrum, but rather Arbitrum plus a monthly supply event that does not care about sentiment, liquidity, etc.

That is how you get a token that can feel permanently heavy even when fundamentals improve, and the chart tells the tale much better than any words of mine can.

That is the tomb.

Aptos (does not look good here)

Aptos is another useful example because the schedule is explicit and long dated.

Messari notes that from April 2024 through September 2026, 11.31 million APT, about 1.1% of the genesis supply, unlock on the 12th day of each month.

Again, you can like Aptos or not. That is not the point (and you can DM me whenever for thoughts on Aptos).

The point is that when the unlock is large enough relative to natural net inflows, the token trades with an embedded headwind.

A chunky unlock vs a four year drip

Most people fear the cliff because they imagine a single day where insiders dump on everyone and the chart dies, which can happen. Sometimes it does.

But the market is surprisingly good at digesting a known shock, especially when it is clearly communicated and when sophisticated recipients hedge.

The data suggests that for larger unlocks, prices draw down into the event, with declines accelerating in the final week. After the unlock, prices tend to stabilize within roughly 14 days, returning to neutral.

This is not to say that every cliff is bullish after two weeks. It is how markets often process anticipated shocks. A cliff has a psychological benefit that a monthly unlock doesn’t: it ends.

It gives the market a chance to clear, it gives buyers a line in the sand, and it gives sellers a moment to de-risk. It also gives the protocol a singular event to generate hype around. Protocols like Ondo have organized entire investment days around their chunky unlocks.

A monthly unlock does the opposite. It keeps the fear fresh.

What happens when you go max chunk?

PUMP pushed price discovery to an extreme. The sale itself was a chunky event. Pump.fun raised about $500M in around 12 minutes, with about 33% of the tokens allocated to the ICO. These tokens were fully unlocked from day one, with no one left wondering what the private round vesting will look like several years from now.

Pump.fun also leaned into buybacks, leveraging the revenue generated from their exchange and frontend and creating a structural bid to counteract initial selling.

It’s important to note that compressing supply problems does not automatically create value. A token can still be overvalued, and PUMP’s token still fell below its ICO price, but the token has been much more stable than many of its peers. They are also much closer to price discovery than many of the low float, high FDV tokens in crypto.

Low float, high FDV

The four year monthly unlock is not an isolated problem. It is a symptom of a broader design pattern: launch with low float, demand a high fully diluted valuation, then let supply creep out for years.

CoinGecko found that low float crypto makes up 22% of large cap tokens, and that for many assets, the majority of token supply has yet to be unlocked, creating ongoing supply overhang.

CoinGecko’s 2024 Q2 report highlighted that most hyped 2024 projects launched with less than 20% of supply circulating while demanding high valuations, and as more unlocks occurred, supply flooded the market and valuations dropped sharply for several high profile launches.

Binance Research made a similar point in their report “Low Float & High FDV: How Did We Get Here?” They highlight an estimate of roughly $155B worth of tokens expected to be unlocked from 2024 to 2030 and warn that without corresponding buy side demand, that supply creates selling pressure.

Here is the most brutal part: If you launch at a lofty FDV and then drip supply out for years, you are implicitly betting that demand will grow smoothly and consistently for years.

Markets do not work like that. Demand is lumpy, liquidity is cyclical, and attention is fickle.

You end up trying to grow into a lofty valuation while the market repeatedly anchors you to a lower one. Once a token anchors lower, it changes everything. New buyers look at the chart and feel like something is wrong, builders feel underappreciated, governance becomes more contentious, treasuries become less powerful, and ecosystem incentives become weaker.

And yes, early investors suffer too, because they are forced to distribute into a market that is structurally conditioned to expect selling. For some reason they get all of the blame, despite sharing the discomfort equally.

Taking your medicine all at once

I am not arguing that every project should do a 100% circulating supply launch. That is not realistic for most teams and most cap tables, and frankly might cause even more problems. I certainly think vesting is inexorably good for all relevant parties.

I am arguing that we should stop treating the four year monthly unlocks as the “responsible” default.

If you want the token to have a chance to be owned by new participants, you need to minimize the period where the dominant narrative is future dilution.

Some principles that feel directionally correct to me:

- Compress the painful period.

- If insiders need liquidity, front load it. Shorten the duration. Finish the uncertain part sooner, even if that means the early months feel worse.

- The market can recover from a shock, but it struggles to recover from a drip.

- Use cliffs for price discovery, then get out of the way.

- Build investor days and big moments out of these days, much in the same way that public companies do.

- Separate team compensation from reflexive sell pressure.

- If the team needs to sell the token to pay the bills, the token becomes a payroll token. Payroll tokens get sold.

- If you must do linear unlocks, make them short and purposeful.

- Linear unlocks can make sense for ecosystem programs where the tokens are being deployed into incentives, liquidity, or builder grants that create demand, but even then you’d likely be better off creating objective or hurdle-based unlocks.

- Large unlocks often stabilize within roughly 14 days after the event, which is a much healthier path than teaching the market to expect selling every month until morale improves (and dealing with the same 14 day period regardless).

- Stop anchoring the public market to a fantasy FDV.

Escape the catacombs

In my “Infinite Game” piece, I wrote about crypto as hope, as something people play because the existing system feels rigged and because they want a game with possibility.

Long monthly unlock schedules quietly destroy that possibility. They train buyers to be cynical, they restrict new participation, and they anchor prices lower. They are a tomb of our own design.

If we want tokens to be owned, not just traded, we have to stop rationalizing drip unlocks and start optimizing for what the marginal buyer actually experiences. We also need to stop Eric Adams from interacting with blockchains.

Sometimes the best thing you can do with pain is get it over with.

The content provided herein may include information regarding past and/or present portfolio companies or investments managed by Blockchain Capital or its affiliates and are provided for illustrative purposes only. The views expressed in each blog post are the personal views of each author and do not necessarily reflect the views of Blockchain Capital and its affiliates. Neither Blockchain Capital nor the author guarantees the accuracy, adequacy or completeness of information provided in each blog post. No representation or warranty, express or implied, is made or given by or on behalf of Blockchain Capital, the author or any other person as to the accuracy and completeness or fairness of the information contained in any blog post and no responsibility or liability is accepted for any such information. Nothing contained in each blog post constitutes investment, regulatory, legal, compliance or tax or other advice nor is it to be relied on in making an investment decision. Blog posts should not be viewed as current or past recommendations or solicitations of an offer to buy or sell any securities or to adopt any investment strategy. The blog posts may contain projections or other forward-looking statements, which are based on beliefs, assumptions and expectations that may change as a result of many possible events or factors. If a change occurs, actual results may vary materially from those expressed in the forward-looking statements. All forward-looking statements speak only as of the date such statements are made, and neither Blockchain Capital nor the author assumes any duty to update such statements except as required by law. To the extent that any documents, presentations or other materials produced, published or otherwise distributed by Blockchain Capital are referenced in any blog post, such materials should be read with careful attention to any disclaimers provided therein.

.png)

.png)

.png)

No Results Found.