.png)

The Hidden War Over Your Stablecoins

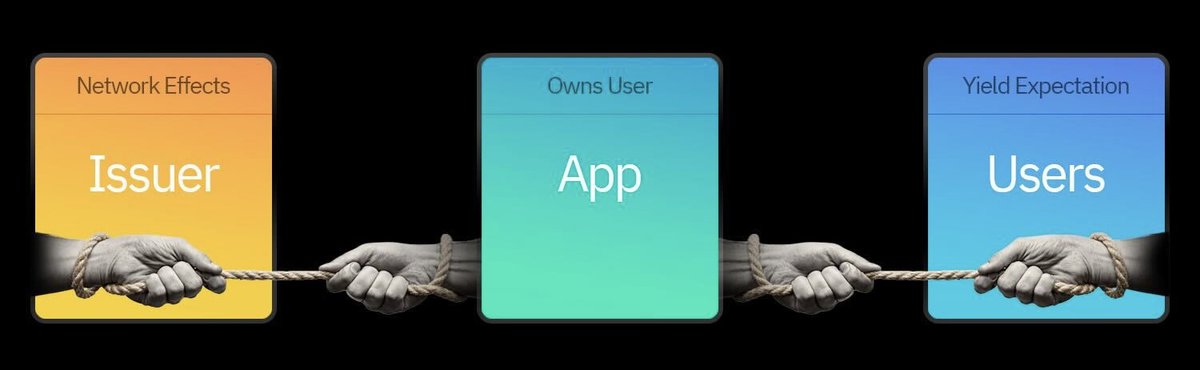

Stablecoin issuers have one of the most profitable business models on Earth, and all of that profit creates an unwanted target. At Blockchain Capital we've had a front-row seat to what has become a three-way tug-of-war between issuers, applications, and users over the profits.

We've backed some of the major issuers (Tether, Circle, Paxos) and several of the applications fighting for a cut (Aave, Phantom, Polymarket, RedotPay, etc.). This is what we're seeing…

Issuers Have It Good

A user sends an issuer fiat dollars, the issuer mints digital dollars on the blockchain. Behind the scenes, the issuer parks the fiat in cash or cash equivalents and earns the risk-free rate. That's the entire business. Banks take your deposits and have to lend them out, manage credit risk, and maintain branches. Insurance companies collect premiums but eventually have to pay claims. Stablecoin issuers basically just hold T-bills. They get the cash flow without the complexity or risk. Revenue scales with assets under management, while operational costs remain roughly constant: a pure, unencumbered cash flow machine. Tether reported $10B in profit in 2025 with a team of ~300 people. This is arguably one of the best business models ever. But all that profit attracts attention.

Applications Want Their Cut

Most users never talk to an issuer. They interface with stablecoins through applications like Phantom which own the user relationship.

Major exchanges, large DeFi protocols, and prominent wallets appear to have meaningful bargaining power with issuers. They can designate the default stablecoin and integrate or deprecate a stablecoin with a single product decision, giving them leverage over where the float flows. If billions of dollars of a stablecoin sit inside one app, that app can ask the issuer for a share of the float. The pitch is simple: we are distributing your asset and anchoring user behavior around your token, so you must share the economics or we will push users toward a competing stablecoin.

This is already happening. The canonical example is Coinbase's relationship with Circle. In the early days, Coinbase was the primary distribution engine for USDC and negotiated a favorable split of the interest income on reserves. It is reported that Coinbase receives 100% of the interest income from USDC held on Coinbase and 50% from USDC held off-platform. We are beginning to see applications both in and out of our portfolio run this strategy and aggressively negotiate for their share.

Branded Stablecoins: Cutting Out the Issuer

Apps can also try to cut out issuers entirely with their own branded stablecoins or wrappers. Instead of routing users directly into USDC or USDT, they can surface a dollar balance that is backed by some combination of stablecoins and short-term instruments behind the scenes. At that point the distributor has partially stepped into the issuance business themselves. Aave's GHO stablecoin is a great example of this phenomenon.

Often, though, applications do not have the resources or licenses necessary to build full issuance infrastructure, so they white-label an issuer-as-a-service solution. Paxos is a flagship white-label provider today, and powers PayPal’s PYUSD. This allows PayPal to monetize the float without having to negotiate with the large issuers.

Issuer Leverage

Applications don't have complete power over issuers. Incumbent stablecoins like USDC and USDT have strong network effects. They are the reserve asset across DeFi and the base pair for most on and off ramps. A branded stablecoin is arguably inferior for users because it has thinner liquidity and fewer integrations.

Furthermore, white-labeled stablecoins are not neutral infrastructure in the way USDT aspires to be. A company competing with PayPal at the app layer may be reluctant to accept PYUSD, since doing so helps a rival. The same dynamic arguably affected Circle in the early days, as exchanges like Binance probably were hesitant to lean into USDC given its close ties to Coinbase, which is why they instead defaulted to USDT. Now USDT has ~5x more trading volume than USDC on Binance.

Users Demand Float

User expectations around yield can create pressure on issuers and applications in developed markets. With risk-free rates around 4%, US users might naturally ask why their digital dollars earn nothing. When one wallet offers yield while a competitor offers zero, users might flock to the former.

If that expectation sets in, applications will find themselves in the middle. To stay competitive, we expect they may have to pass some of the float back to users, which will force them to negotiate harder with issuers. An application that cannot secure a share of the yield has little room to pay interest to users without burning its own cash. As more products market yield on stablecoin balances, it becomes harder to defend the neat issuer-centric model where all of the float stays at the bottom of the stack.

This pressure is not universal. In many foreign markets, the primary value of a dollar stablecoin appears to be protection against local inflation and currency controls rather than yield optimization. A user trying to avoid losing half their purchasing power each year is probably far less focused on whether they earn 4% on their dollars. For global issuers with deep penetration in those regions, user demand for the float seems less of an immediate concern than it is for domestic issuers competing for US depositors. We believe this dynamic may favor Tether, which has one of the largest foreign user bases.

Conclusion

Taken together, user expectations and issuer economics put applications in a tight spot. They are caught in a tug-of-war between users who now expect to see yield on their stablecoin balances and issuers who still want to keep most of the float. The stablecoin stack is evolving quickly, and the division of profits is still being negotiated. My guess is that users may be the ultimate beneficiary of the tug-of-war and end up with most of the yield. In a following article, we'll explore other business models applications are building around stablecoins.

Thank you to Cole and those at Blockchain Capital who gave invaluable feedback on the article.

Blockchain Capital may be an investor in one or more of the protocols or companies mentioned above. The views expressed in each blog post may be the personal views of each author and do not necessarily reflect the views of Blockchain Capital and its affiliates. Neither Blockchain Capital nor the author guarantees the accuracy, adequacy or completeness of information provided in each blog post. No representation or warranty, express or implied, is made or given by or on behalf of Blockchain Capital, the author or any other person as to the accuracy and completeness or fairness of the information contained in any blog post and no responsibility or liability is accepted for any such information. Nothing contained in each blog post constitutes investment, regulatory, legal, compliance or tax or other advice nor is it to be relied on in making an investment decision. Blog posts should not be viewed as current or past recommendations or solicitations of an offer to buy or sell any securities or to adopt any investment strategy. The blog posts may contain projections or other forward-looking statements, which are based on beliefs, assumptions and expectations that may change as a result of many possible events or factors. If a change occurs, actual results may vary materially from those expressed in the forward-looking statements. All forward-looking statements speak only as of the date such statements are made, and neither Blockchain Capital nor each author assumes any duty to update such statements except as required by law. To the extent that any documents, presentations or other materials produced, published or otherwise distributed by Blockchain Capital are referenced in any blog post, such materials should be read with careful attention to any disclaimers provided therein.

.png)

.png)

.png)

No Results Found.