.png)

The Great Consolidation

We did this to ourselves

As crypto is thrust again into the center of global attention, we sit at a pivotal moment in our industry. We must consolidate the ecosystems, consolidate the apps, and consolidate the memes. Consolidation is the way.

Bitcoin began as a disruptive technology designed to usurp modern banking and put the power of self-custody back in the hands of the people. It was designed to be a hedge against burgeoning centralization and rampant inflation, and its power increased as consensus around its value grew. Programmatic scarcity – the 21 million hard cap – has become more and more attractive as digital gold looks to replace its older, physical counterpart.

Over the past year, we’ve seen an explosion of Bitcoin interest and adoption. We’ve crossed $100k per coin and recently hit all-time-highs, we’ve seen Bitcoin thrust back into the global spotlight, and countries are now buying it while discussing the possibility of creating their own national reserves. The current President of the United States is talking about making America the “crypto capital of the planet.” As Bitcoin has risen, it’s carried the entire crypto industry with it, with crypto boasting a $3.78 Trillion market cap today. We’ve come a long way.

In many ways, things could not be going better for crypto. For the first time in the history of our industry, we might actually have regulatory clarity and support as the SEC softens its stance and bills start to pass. We have Larry Fink embracing the future of tokenization. There’s actually real things happening instead of this loose concept of a Metaverse that will never get built or jpegs on an IPFS server. It’s actually being taken seriously (though not by everyone, not even really by most), and this seriousness ramps up every time governments print money or markets fall into turmoil.

Memecoins, perps, and tokenized stocks are being added to tradfi platforms like Robinhood. Something is happening, dare I say.

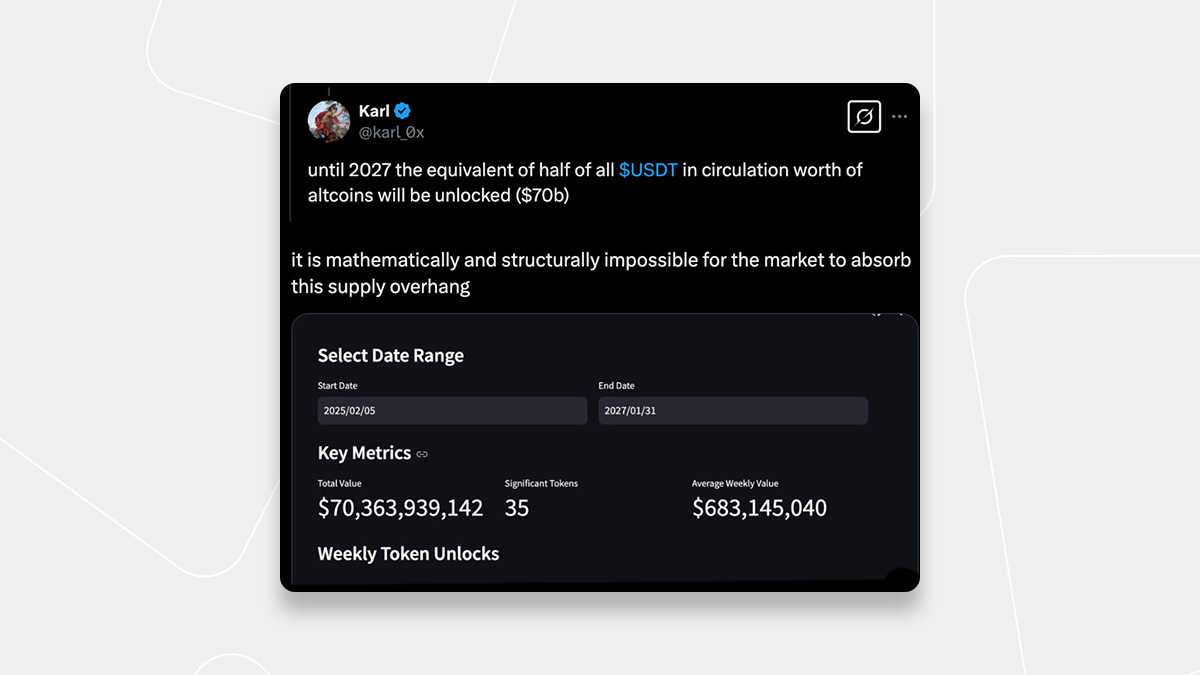

Despite the wins, there is still a lot of wood to chop when it comes to crypto, and a storm is brewing as over $70B of altcoins become unlocked, funds begin to harvest as they look to return capital to investors, and true price discovery happens absent of low float, high FDV launches. We have already gotten a small taste of what this looks like, with many alts down 50-70% from their prior highs. Many of these protocols launched tokens without a strong (if any) PMF, chased speculative hype, and will likely not survive a prolonged bear market. The token was the product, and the product stinks.

The Great Consolidation is upon us, and it’s coming a bit faster than you think.

Taking out the trash

Today, our industry is largely getting the recognition and attention we have always felt it deserved. Prior cycles often overextended and overestimated the state of the technology and its potential. We have had to lean on speculation and FOMO to drive attention, and this has created an air of distrust and skepticism that worsens with each cycle. I’ve long said crypto attracts your best and worst friends, and this seems universally true.

For the first time, we have the opportunity to make good on the promises made long ago. Bitcoin thankfully doesn’t need to do much, given that its value accrual lies with its programmatic scarcity. Outside of Bitcoin, however, lies a veritable chasm. Take a run through the top 100 today, and you will see a tremendous amount of garbage sitting alongside real, innovative projects. In a post-tariffs world, Cardano is still worth $28B US dollars. We deserve hellfire.

A lot of people have called attention to the rise in memecoins as a burgeoning issue for crypto credibility, and I think what these people miss is that memecoins sit in a different mindspace than the rest of the crypto market. They are financially nihilistic by design, everyone knows they are destined to go to zero, and are, by and large a product of the true issue: we have long propped up shoddy, copycat ecosystems and directly undermined the future of our industry for a long time. We have made a meme out of everything, and blame the user for not being able to tell the difference.

We have incorrectly fostered distrust in VCs, given rise to billion-dollar whitepapers with no product, and incentivized short-term extraction over long-term value creation. The system largely works in favor of insiders instead of the users who make the protocols valuable, and memecoins provide users with a synchronous game largely free from insider dumping and misaligned incentives.

Moreover, memecoins are almost entirely fully unlocked and don’t obfuscate the true value behind low float, high FDV financial games. They are blissfully unattached to fundamentals, and seemingly the more that devs try to do (e.g. building an L2, launching products, etc), the worse the coin performs. They are not the problem, given that most users are drawn to them because of issues in our industry. At least, they worked for some time before greed and centralization ruined that game for most people.

Alt szn?

Historically, Bitcoin dominance wanes after big up moves, leading to what we call “alt season,” a time in which alternative coins see meteoric gains as traders pile into high-beta assets. This has not happened in the current cycle, as Bitcoin dominance has trended higher and higher, and most alts have seen massive corrections. Outside of retail demand for memes, this is in large part due to institutional demand being limited primarily to Bitcoin ETFs, with markedly smaller flows into Ethereum ETFs. The average new entrant into crypto does not want to have to read whitepapers or decide which L2 is going to win; they want to keep things simple, and Bitcoin is already a high-beta, risky asset to them. Bitcoin is outperforming, compounding, and consolidating speculative capital.

There is a massive wave of unlocks coming for altcoins, with about $70B of coins coming into circulation between now and 2027, and it remains to be seen who the marginal buyer will be for the majority of these assets as liquidity dries up and retail interest is fragmented by ecosystem and token.

Another reason we have yet to see a real alt season like we have in prior cycles is the fragmentation of liquidity across chains and tokens. Even after pump.fun revenue has dropped by 70%, there are still 25k+ tokens being launched every single day (226 of which have graduated, with the highest market cap not even reaching $1m). This is entirely unsustainable, as the casino hasn’t been designed for retention. The Infinite Game has become "Finite", and people are leaving the casino (or being forced out).

Retail traders attracted to asymmetric upside opportunities, the Infinite Game, and hypergambling are much more likely to buy memes or majors that they know and understand than try to make sense of a whitepaper that addresses a problem that doesn’t exist or that they don’t understand. Crypto natives are hyper-aware of the low float, high FDV games being played by the majority of projects, and are uninterested in becoming exit liquidity for VCs.

Real projects are caught in a difficult place because their valuations aren’t that much more attractive given inflationary (albeit necessary) funding rounds, and the number of marginal buyers has declined substantially. Moreover, the rise of Echo.xyz and retail-oriented rounds has further democratized access to private rounds, leaving even fewer buyers after TGE. Major exchanges have also chosen largely to forego listing quality projects in lieu of memecoins, as Coinbase only had 18 day one listings in 2024.

In short, and I can’t believe I’m saying this, there are simply too many tokens in circulation, and WAY too many tokens still to be unlocked in the near future. There is no other direction for the market to go, and there isn’t enough liquidity to sustain these valuations. Consolidation is the only way.

How does consolidation work?

Consolidation, as I see it, should come in many forms.

Consolidate the Memes

In the meme ecosystem, dollars will coalesce around the biggest, most globally understood memes (Fartcoin comes to mind), with a high preference for more “lindy” names that have withstood multiple cycles, and the “daily runners” will become increasingly EV and ephemeral. We saw this happen for the first time when President Trump launched his $TRUMP coin, creating a black hole for liquidity that kicked off the death spiral of many memes. This also revealed that the giant ball of money in crypto was not nearly as big as it might seem, and that money needed to flow into fewer assets.

Bear in mind that consolidation is healthy, given there are very few flash-in-the-pan cultural phenomena that should command centi-million-dollar valuations.

Memecoins should, ideally, shift towards more synchronous time games that users can speculate on. This should take a slightly different form than today, where coins slowly bleed out as people move on to other games. Somewhere out there, someone still holds chillguy, and that game ended a long time ago. Much in the same way that the NFT space got increasingly more PVP and extractive, memes have ultimately hurt their users more than helped them, and until this space consolidates, it will continue to be a cemetery for hopefulness.

Crypto will continue to be the best place to trade events, cultural zeitgeists, and monetize one’s pulse on the present, but it will have to look much different to exist sustainably, and there will certainly have to be less coins. I have little doubt that we will always find a game to play, but anyone who has ever played a massively online multiplayer game understands that the game is substantially less entertaining when there’s no one on the server.

Memes consolidating will allow for a much more friendly environment for risk-on degens, creating a wealth effect that has historically been positive for DeFi and other onchain activities. Study WIF, BONK, DOGE, etc, and what these did for the rest of crypto.

Consolidate the ecosystems

The past few cycles have all rewarded builders who fork successful protocols and bring them to new ecosystems. The Alt-L1 trade has been one of the best trades in crypto, and these underlying ecosystems have all raised significant venture funding while building piecemeal improvements on what already exists. This is unsustainable, and this game ultimately robs our future in the same way drinking 11 Modelos on a Saturday night robs my Sunday.

Let’s take a look at Aptos, currently valued at ~$6B. Take a spin through their ecosystem and let me know if you see any unique applications. I’ll wait. What things can you do in this ecosystem that you can’t do in dozens (read: any) of others?

Pick your favorite (or least) ecosystem and do the same exercise. We have become like rats addicted to cocaine, where we prioritize cheap hits and time to liquidity over sustainable businesses and true innovation. We need fewer copycats, fewer dollars wasted on thinly veiled TGE games, and fewer instances of the fraud and bad behavior that comes with it.

Successful ecosystems will provide a unique value proposition to their users and developers. The more loyalist, cult-like ecosystems (think Solana, Berachain, Hyperliquid, etc.) will likely survive due to the increasingly PVP / tribal nature of the industry during sustained bear markets, but the era of all-vibes-no-fees is likely nearing its end, and performance improvements are fairly marginal at this point.

Solana is, as many would say, in an “interesting spot” because they’ve by design consolidated activity around a few key protocols and have seen true winners emerge in DeFi. It remains to be seen how many users can be retained, but users aren’t that fragmented in the ecosystem today. It doesn’t appear that this is under real threat, and Solana has had the second mover advantage relative to Ethereum, enabling them to avoid many of the same pitfalls while moving towards an aligned goal of IBRL. This cannot be said of many other ecosystems.

Consolidate the apps

Toly famously once said that there are only six essential smart contracts that exist in crypto today. Whether you agree with this take or not, it does stand to reason that there exists a tremendous amount of redundancy in crypto, which has stalled innovation and progress. Even worse, most apps have failed to expand meaningfully beyond their initial value proposition. Fat applications looking like Ozempic hit them.

Users across the globe are accustomed to feature-rich applications—superapps where they can do everything that they need (see WeChat, etc). They shouldn’t have to go to one place to borrow/lend, another to swap, and another to yield farm, and given that the frontend owns the user-relationship, it stands to reason that applications that have real users and traction will continue to broaden their scope to capture more value, especially given how little barriers to entry are. We’ve seen this happen with Jupiter and many other projects that have established dominance in a particular vertical. Many of these are even becoming their own L1s entirely to capture more fees, though it remains to be seen how much value this truly adds to the user outside of its impact on token price. The race to super app supremacy is about consolidating the competition before they consolidate you.

Like in the real world, farming has become increasingly unprofitable for the solo user, and the only apps that gain real, sustainable traction today are either meaningfully improved versions (Hyperliquid) or entirely net-new (pump.fun), and this promotes positive innovative pressures in our industry that will allow it to flourish.

What happens to Ethereum?

Anyone who follows me knows I’ve often had a bone to pick with Ethereum maxis, L2 fragmentation, and questionable value accrual and “moneyness.”

For the Ethereum asset to be valuable, either the L1 needs to accrue the most value as the global settlement layer, or Ethereum as an asset needs to become the cheapest de facto “money” of the ecosystem. The former is relatively easy to value, while the latter can take a much higher and more irrational multiple.

As L2 activity has picked up, the fee story for Ethereum as settlement layer has been largely underwhelming, with ETH only being paid ~1% of all fees on Base. When you consider the fact that even ETH block space demand is also declining, it’s hard to find a scenario in which Ethereum is able to outperform any of the major L2s in its network, although each of those tokens also struggles to tell a meaningful value accrual story themselves. In fact, Base, the leading L2, succeeds in spite of no token. You’d need 100x activity across all L2s just to be at parity with where they are now (and while leaking 99% of the economics to other players in the ecosystem).

There is a case to be made that ETH is still valuable as money, but the rise of stablecoins and the drop in gas prices directly threaten this narrative. BTC is used more as collateral than ETH on Morpho, for instance. This is a negative feedback loop that has hindered institutional demand for the EthTF, given that a lot of the focus centers around Ethereum as a yield-bearing asset, and it’s a $150B asset that doesn’t have a clear narrative around value accrual. In a way, the rise of stablecoins threatens the token narrative of many new projects that must justify their existence now more than ever.

What’s worse, users have been heavily fragmented as L2s amass massive war chests and grant programs incentivize weak, quickly shipped applications with heavily-sybilled user bases and lackluster PMF. Base’s “onchain summer” has devolved to Jesse Pollack chasing people down on the street and begging them to accept $50, promoting cheap meme pump and dump derivatives, and saying that “Base is for pimping." ETH/BTC has fallen to levels it has not seen in years, and Ethereum has seen much stricter competition for developers and block space than ever before.

Who will save ETH? This question has largely gone unanswered as the EF argues about nebulous nonsense that no one cares about, and chain usage dwindles. There is more Ethereum blockspace than ever, and nary a demand to fill it. There are meaningful cultural, financial, and technological problems.

The good news is that a Great Consolidation flattens copycat ecosystems, causes a mass exodus of mercenary users and developers, and pushes value towards actually useful applications. It forces Ethereum to solve its problems immediately or face further devaluation against its competitors. “Just use Aave” extends to many of the biggest and most successful applications on Ethereum, and gives it a fighting chance to attract liquidity, institutional adoption (in which it currently dominates), and maintain its position as the leading smart contract platform.

Blobs are long-term bullish for Ethereum’s scalability and should increase Ethereum fee capture over time as more ETH is burned. There’s also always the option of putting "tariffs" on the L2s and reorganizing the model in a way that favors the L1 a bit more equitably than what exists today. The key to success here is that the Ethereum ecosystem will need to continue to be the most developer-rich ecosystem in crypto, driving exponential demand onchain. Only then will they be able to stave off competition and maintain pole position.

The bad news is that there doesn’t seem to be an agreement on value accrual for Ethereum yet, and consolidation into L2s still undermines value accrual to Ethereum as an asset. If everyone goes to MegaEth, for instance, value will accrue to MegaEth. Celestia also threatens them on data availability, as mamo-1 enables 683x Ethereum’s blob target. There’s a lot of wood to chop.

Another large concern is that the unravelling of Ethereum low float, high FDV as these tokens come unlocked and discover their real price will have a cascading negative effect on Ethereum overall, given the amount of alts that sit in lending protocols and how many of them need to sell their own tokens in treasury to make payroll, etc. If these protocols cannot find real revenue streams or marginal buyers, they will put further downward pressure on Ethereum. Users need a reason to buy and hold Arbitrum, and the lack of narrative extends all the way down throughout the ecosystem.

Who wins?

Protocols that are able to generate meaningful fees and secure high-margin revenue should rise to the top as fundamentals become more important and speculation wanes.

Protocols like Aave and Ethena generate meaningful revenue, are highly trusted by their user bases, and have seen their market shares rise even if their token prices have been volatile. Uniswap is going the Unichain route, expanding its value capture and improving its revenue profile, though it remains to be seen how much the market values this (it certainly didn’t benefit DYDX). Hyperliquid is exploring the app-led L1 ecosystem, generating more in fees than most of its competitor L1s and absolutely dominating the perps landscape. You don’t need me to spell out that story, just go on Twitter for 5 seconds and you’ll see it.

It will be very interesting to see how the supply overhang plays out with alts that launched low float tokens before they established sustainable revenue streams. Protocols that are largely through their distribution and vesting phase and generating meaningful, sustainable revenue will start to look more attractive as their cost structures come down and price action stabilizes. Those who haven’t will experience pain as investors fly towards safety. Recent price action in $OM shows what is possible, if the foundation of a protocol is built on hype and sand. Most days, the weather is nice, but be careful what you are holding on to when the wind blows.

For what it’s worth, I remain highly constructive on crypto and think there are venture-scale opportunities all over the place. Consolidation is incredibly important and healthy, and I look forward to real innovation and development. I will continue to monitor pair trades, and my eyes will remain glued on the charts.

Blockchain Capital is an investor in one or more of the protocols mentioned above. The views expressed in each blog post may be the personal views of each author and do not necessarily reflect the views of Blockchain Capital and its affiliates. Neither Blockchain Capital nor the author guarantees the accuracy, adequacy or completeness of information provided in each blog post. No representation or warranty, express or implied, is made or given by or on behalf of Blockchain Capital, the author or any other person as to the accuracy and completeness or fairness of the information contained in any blog post and no responsibility or liability is accepted for any such information. Nothing contained in each blog post constitutes investment, regulatory, legal, compliance or tax or other advice nor is it to be relied on in making an investment decision. Blog posts should not be viewed as current or past recommendations or solicitations of an offer to buy or sell any securities or to adopt any investment strategy. The blog posts may contain projections or other forward-looking statements, which are based on beliefs, assumptions and expectations that may change as a result of many possible events or factors. If a change occurs, actual results may vary materially from those expressed in the forward-looking statements. All forward-looking statements speak only as of the date such statements are made, and neither Blockchain Capital nor each author assumes any duty to update such statements except as required by law. To the extent that any documents, presentations or other materials produced, published or otherwise distributed by Blockchain Capital are referenced in any blog post, such materials should be read with careful attention to any disclaimers provided therein.

.png)

.png)

.png)

No Results Found.